The Canada Revenue Agency has announced upcoming changes to help process Disability Tax Credit applications more efficiently and reduce delays for applicants.

The Disability Tax Credit, commonly called the DTC, is an important non-refundable tax credit that helps individuals with disabilities, or their supporting family members, reduce the amount of income tax they may have to pay. To avoid delays, applicants should make sure they are using the correct application method and the most current version of the required form.

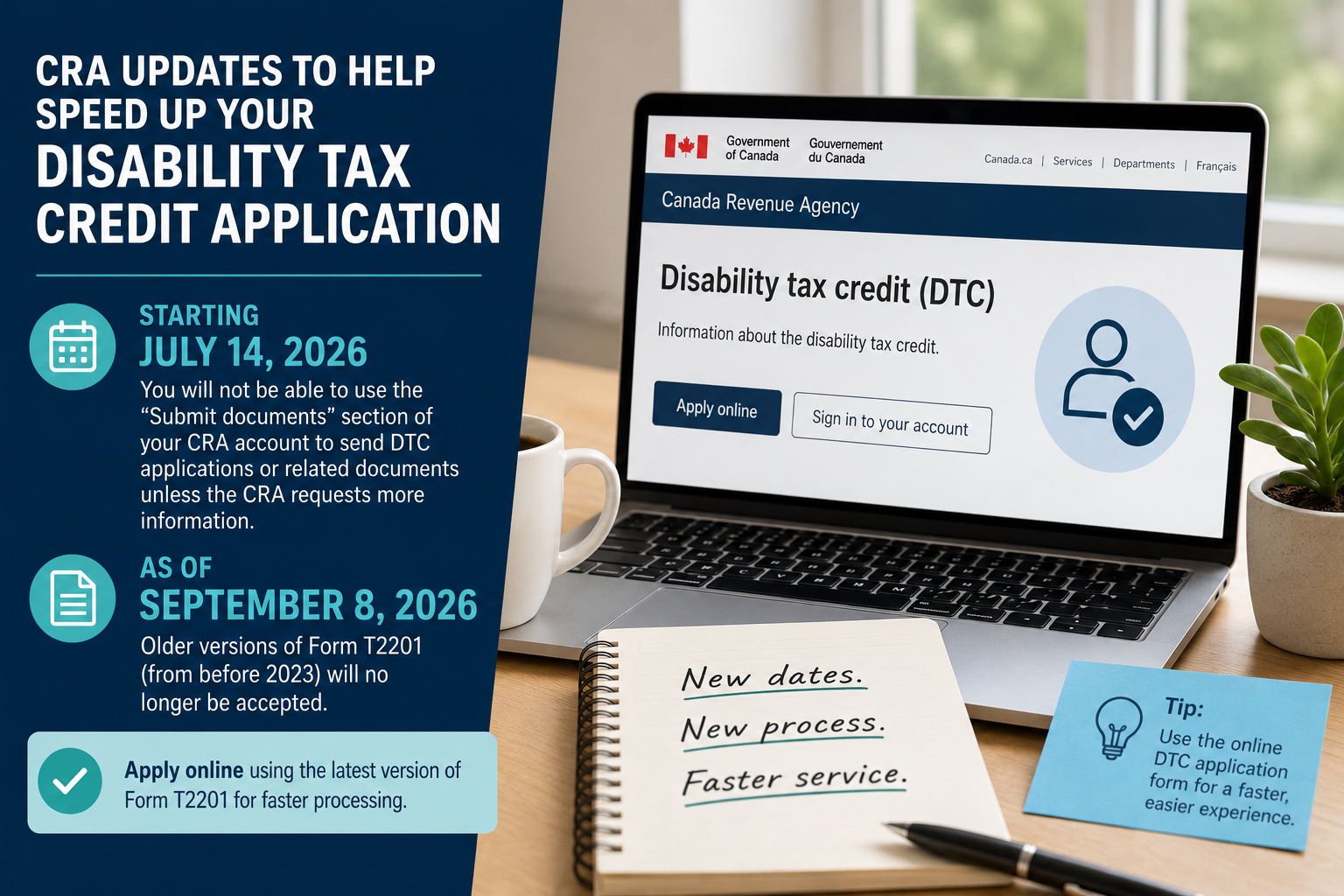

Key Dates to Know

Starting July 14, 2026, applicants will no longer be able to use the “Submit documents” section of their CRA account to send new DTC applications or related documents, unless the CRA specifically requests additional information.

As of September 8, 2026, the CRA will no longer accept older versions of Form T2201 from before 2023.

Apply Online When Possible

The CRA recommends applying through the online DTC application form in your CRA account. Online applications are generally processed faster than paper applications and help reduce common errors.

The online form is always the most current version and is designed to help applicants complete only the sections that apply to them. It also allows both the applicant and their medical practitioner to access the form online, making the process more efficient.

Do Not Use “Submit Documents” for New Applications

The CRA has clarified that the “Submit documents” feature should not be used for new DTC applications.

This section is only intended for providing extra information when the CRA requests it for an existing application or case. If the CRA needs more information, they will contact the applicant through their CRA account or by mail. The request will include instructions and a case reference number.

Paper Applications Are Still Available

Applicants who prefer to apply by paper can still do so, but they must use the latest version of Form T2201, dated 2023 or later.

Once completed and signed by both the applicant and the medical practitioner, the form should be mailed to the appropriate CRA tax centre.

Beginning September 8, 2026, applications submitted using versions of Form T2201 from before 2023 will not be accepted. Applicants using an outdated form may be required to submit a new application.

Need Assistance?

If you are applying for the Disability Tax Credit or are unsure which version of the form to use, it is important to review the CRA’s current instructions before submitting your application.

Seniuk & Marcato can assist with tax planning questions related to the Disability Tax Credit and help you understand how an approved DTC claim may affect your personal tax return.